In a forthcoming article (‘A T-shirt model of savings, debt, and private spending: lessons for the euro area’, European Journal of Economics and Economic Policies: Intervention, Vol. 13 No. 1, 2016, pp. 39–56), I have discussed the relevance of the savings-debt constraint in macroeconomics, and have argued that EU policies violate the savings–debt constraint. As long as this continues, the euro area will continue to live dangerously and will remain vulnerable to political disintegration.

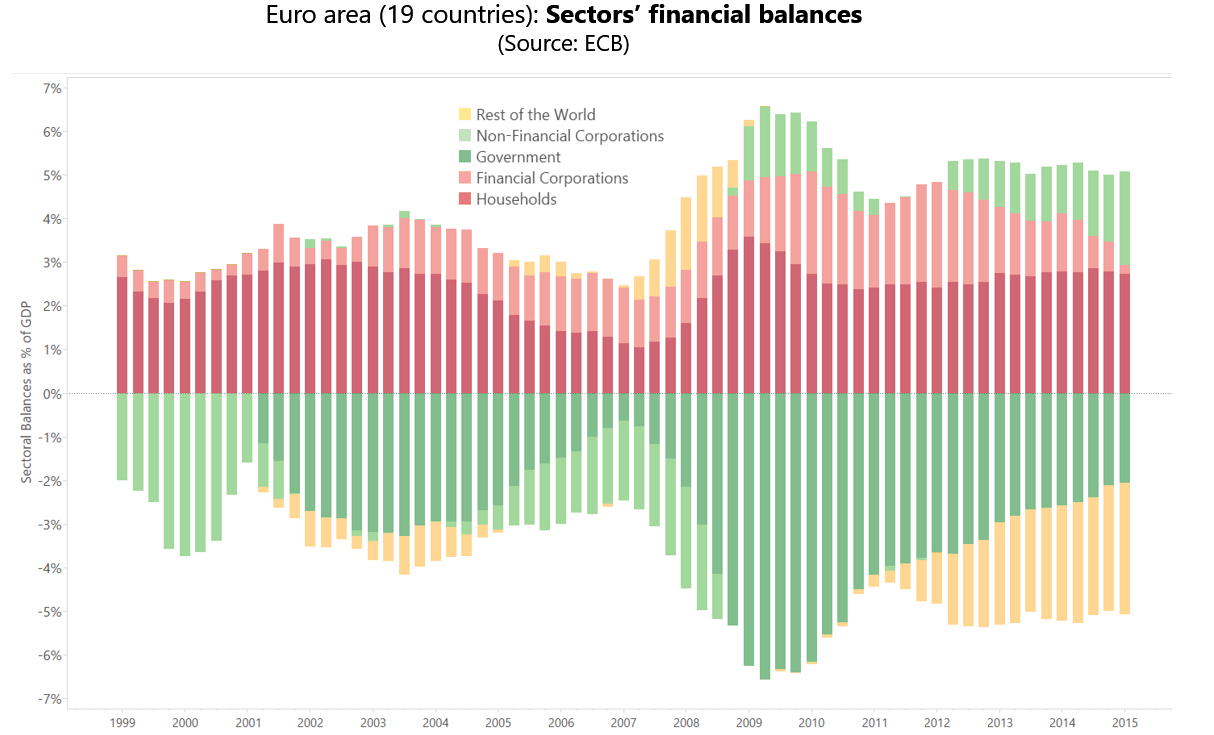

The EU has always stressed that euro area’s national government budget must be consistent with the budget constraint set by fiscal rules, while offering no other channel for fiscal flexibility at the euro area level. This approach is inconsistent with a key constraint in macroeconomics that I call the savings-debt constraint.

In a nutshell, the savings-debt constraint says that any policy that inhibits debt also inhibits financial savings, spending, and jobs. Evidence that the EU policy framework is inconsistent with the savings-debt constraint is offered by the first priority in the list offered online by Jean-Claude Juncker, President of the European Commission: ‘Creating jobs and boosting growth – without creating new debt.’ As long as EU policymakers believe or assert this principle, the euro is in unsafe political hands.

Read more